Decentralized finance, or “DeFi” (as it’s been aptly nicknamed), has been heralded by many as cryptocurrency’s first major use case outside of plain P2P payments, first enabled by Bitcoin. As such, it is now the main focus of developers and investors alike, but there exists precedent for what comes next.

We’re going to analyze what tools we have in the traditional finance sector, versus what has been made available in DeFi today. By making this comparison, we can make additional predictions about what tools come next, further understanding DeFi by referencing commonly known game mechanics that can aid us visualizing how they may come into being, over time.

Today, using decentralized tools, individuals can take out collateralized loans, short different assets, collect interest and even trade on margin. It is eye-opening to many once they realize these things can be done without giving out so much as an email. We have become so accustomed to giving away our data, that using these tools without even logging in to verify your identity to someone seems…off.

Many individuals first experience with this recently has been Uniswap.io, a decentralized exchange built on Ethereum. You simply visit the site and you’re presented with a very simple interface to start creating your own liquidity market or participate in trading with others — all with no real names, or email addresses. It is the same story with many of tools in DeFi, and can feel akin to the first time you interacted with a cryptocurrency wallet and sent your first transaction, kind-of magical.

A Quick Example

Here is a run through of a random scenario showcasing what is possible in DeFi on Ethereum today:

You could send ETH to the MakerDAO protocol to take out a collateralized loan in DAI, a cryptocurrency soft pegged to 1 USD (via a price oracle). You could then use that DAI to buy WBTC (a token with a 1:1 backing with Bitcoin) and take that WBTC and create a margin long position on DDEX.io or then loan it out on Compound to collect interest. At the end of the day you can close all of these positions whenever you want and reclaim your original ETH without ever having lost exposure to it. This can all be done without providing any personal information, and is only a small fraction of what is possible today.

There are, of course, many things we use in our everyday lives with traditional finance that do not yet have a decentralized counterpart, such as short term personal loans (non-collateralized) or mortgages. The trust-less nature of blockchains make the notion of trusting an individual to repay a loan exceedingly complicated. The loans that exist in DeFi today require “over-collateralization” to incentivize users to repay their loans (and provides sustainability to the underlying protocols they’re built upon).

In the real world, this isn’t necessary, because our debts are tied to our legal identities which have their own associated credit scores. It stands to reason that once credit can be replicated on a blockchain, these tools could exist shortly thereafter. Unsecured DeFi loans could take the form of users wallets being treated as speculative assets based on its track record. High risk “new wallets” would be burdened with high interest rates and lower limits (i.e. garnering less lenders).

On the flip side, wallets with a stellar track record would garner much greater interest (higher limits) from speculators and could therefore see lower premiums. As long as the wallets’ reputation has value, it is easy to believe a tool facilitating unsecured loans could exist while retaining users’ anonymity. With that said, what other tools can we anticipate to see in the coming years?

The financial tools and institutions we use today weren’t created overnight, and can be incredibly complex given the years of compounded composability that occurred with legacy markets overtime.

A lot of what we use seems obvious in retrospect, but there was thousands of years between the invention of modern banking and money. There was then another couple of thousands years between banking’s creation and the utilization of paper notes as we know them today. DeFi is following a similar path — albeit extremely accelerated — so we think it’s best to look at these tools like a skill tree since, as so many of us understand gaming; with DAOs and decentralized groups often resembling online guilds and borrowing game-like mechanics, such as “rage-quitting”. Why not continue that tradition and explain DeFi in a similar way?

In your typical RPG (role playing game) you will have a skill tree that looks like this:

Fig 1. A very familiar skill-tree for anyone who played Diablo 2 in the 2000s.

This is a skill tree for Diablo II, and is extremely simple to follow. To get a frost shield that freezes enemies, you first need to learn how to make a frost shield. To get a shield that actually hurts enemies, you need to learn how to make it freeze them; it’s very simple and second-nature to avid gamers. Financial tools are the same way. You can’t have reliable money without it being backed by some form of value (though we can talk U.S. financial policy another time).

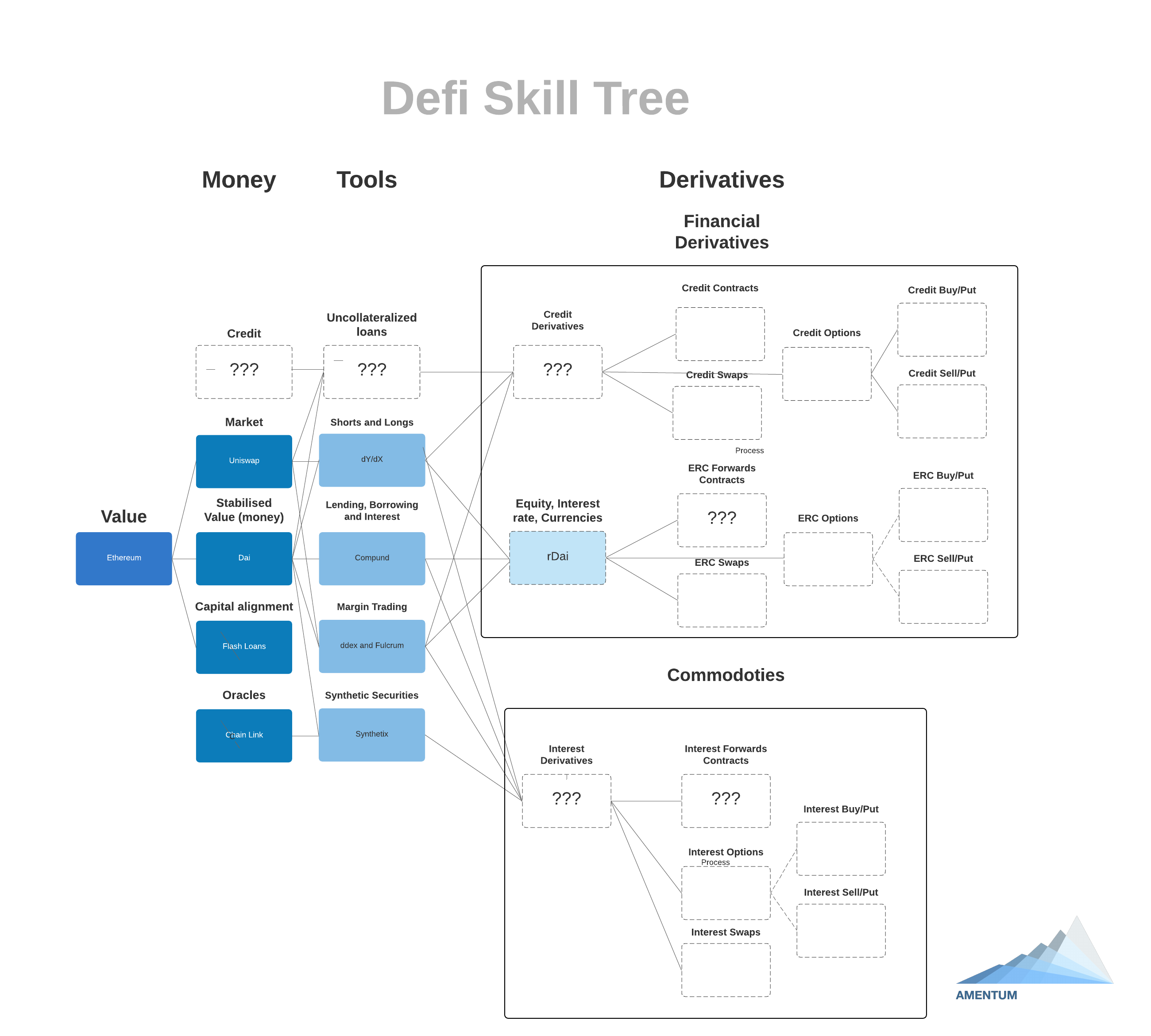

You can’t have loans and interest without money, and without loans and interest you can’t have margin trading. There are a great number of mechanisms and complexities to this, but we have attempted to create a fledgling “DeFi Skill-Tree” to illustrate my point. Using this and extrapolating further, I believe it is possible to predict the next wave of tools we are going to see, as well spot openings for potential new ones.

Fig 2. A modern gaming like skill-tree for potential DeFi growth and expansion. While not an exhaustive list, it’s enough to show you where things are headed.

In the model above, ETH is the source of value — basically the gold in Fort Knox pre-FDR — and DAI is the US Dollar. This may seem counterintuitive to the, “BTC is gold and ETH is oil.” narrative, but I don’t think legacy concepts necessarily apply to the tools we are creating all the time, so let’s be flexible given this example.

In putting this together I noticed a few outliers, namely Uniswap and flashloans, as neither have a legacy market equivalent I am aware of. As we saw a few months ago, the creation of flash loans enabled an individual to make $360,000 out of nothing. This was possible due to the ability for the user to control a very large amount of capital, with no collateral, for the length of an entire Ethereum transaction. This created a wild card the DeFi markets were not properly equipped to deal with. Now that the market is aware of this inefficiency (or efficiency, depending who you ask), new tools will be created with that in mind (i.e. Uniswap V2 allows you to take out flash loans with assets in its liquidity pool, for the length of a transaction as long as the funds are returned in the end).

This trend will continue and evolve into an entirely new branch of finance. Possible future branches could include speculation around market depth itself, or derivatives around the size and potential impact of flash loans.

The big shift in these markets is going to come into play once the real world is “plugged in” using decentralized data oracles. When users are able to speculate on traditional financial markets without the need to touch anything traditional, interest will explode. We will then begin to see DeFi markets emerge around forex, commodities and stocks, as well as the impact these new tools will have on those markets.

Moving Forward

The impending interference of traditional markets from crypto-based ones will add a great deal of liability to the interfaces for these exchanges. Censorship will be imminent. Taking the Uniswap example from earlier, though the mechanisms are decentralized, the domain “Uniswap.io” is very much tied to an individual or organization. If these domains enable users to trade stocks without so much as a first name (basic KYC/AML requirements), they will be shut down.

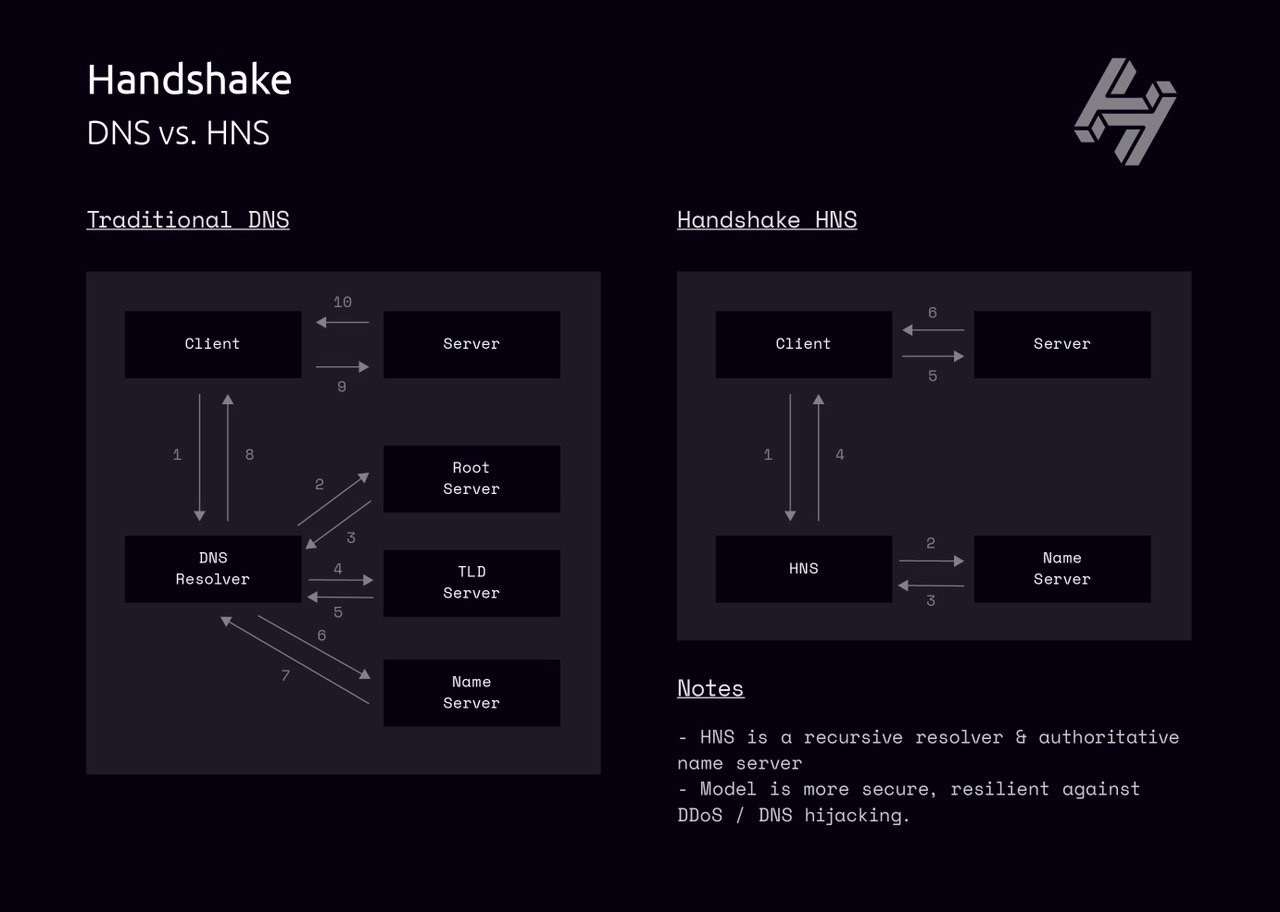

There is a solution however, in the form of Handshake’s decentralized root anchor and DNS alternative. The existence of a blockchain to secure top-level domains is imperative for these tools to flourish in the mid to longterm. You cannot truly have decentralized liquidity, without also coupling that with decentralized access and censorship resistance at the DNS level.

Fig 3. High-level graphic illustration of the HNS network by Darren Mills and Steven McKie.

By allowing users anonymity/pseudo-anonymity and absolute control of their domain names, it will enable the creation of some of the most ambitious financial tools imaginable. With the ability to create DeFi tools and services, without being hindered by the potential legal repercussions even further (see EtherDelta shutdown), developers will be further emboldened to innovate without restriction in how they allocate and programmatically manage digital value.

As it stands today, creating some of the markets we have described would almost certainly result in extensive legal repercussions for those operating in more restrictive financial regulatory climates. With those barriers now being lifted for those who can flexibly benefit from these new technologies, we believe 2020 is going to be an amazing year for DeFi. We are excited to continue building upon this skill tree, iterating on it slowly, as we continue to create the periodic table of finance.